🏠 Bank‑Required Inspections:

FHA, VA, Conventional & Fannie Mae

Understanding Phase 1, Phase 2, and Phase 3 Inspections

Before diving into each loan type, it helps to clarify what “Phase 1, Phase 2, Phase 3” means.

These are NOT federal terms—they are Texas builder/inspector workflow terms used by lenders to verify construction quality before approving a mortgage.

🔧 Texas Construction Inspection Phases (General Definitions)

| Phase | What It Covers | Purpose |

|---|---|---|

| Phase 1 – Pre‑Pour / Foundation Inspection | Soil preparation, formwork, reinforcement, post‑tension cables, plumbing rough‑in | Ensure the foundation is structurally compliant before concrete is poured |

| Phase 2 – Pre‑Drywall / Framing Inspection | Structural framing, roof decking, mechanical rough‑ins (HVAC, plumbing, electrical), window/door installation, WRB, flashing | Verify structural integrity and building envelope before insulation and drywall |

| Phase 3 – Final Inspection | Full home inspection after completion: systems, safety, code compliance, functionality | Confirm the home is complete, safe, and ready for occupancy |

Now, what each loan type requires at each phase.

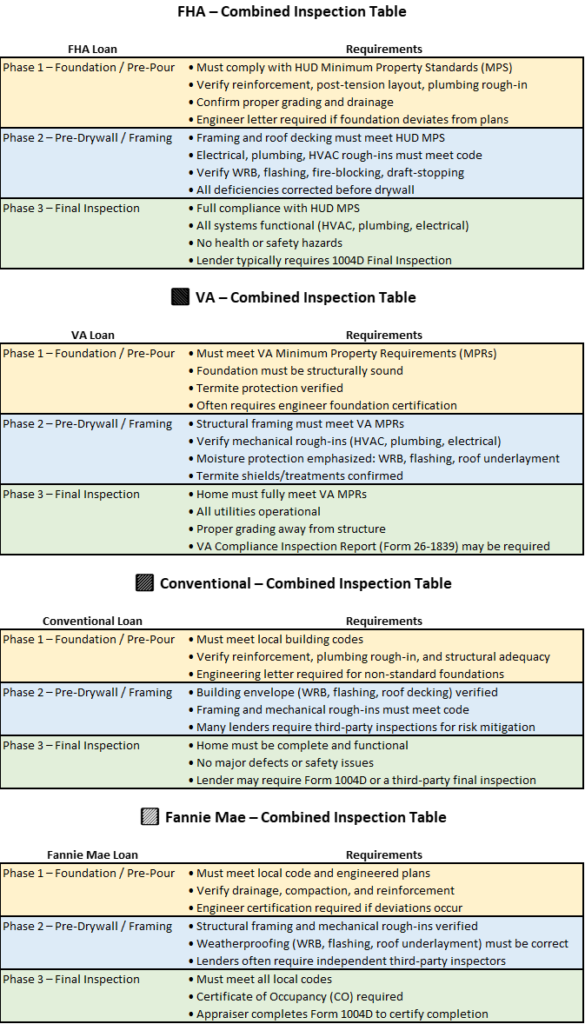

🟦 1. FHA Loan Requirements

FHA = Federal Housing Administration

FHA follows HUD Minimum Property Standards (MPS) and HUD Handbook 4000.1.

Phase 1 – Foundation

- Inspector must verify compliance with HUD MPS and local building codes.

- Special attention to:

- Reinforcement placement

- Post‑tension cable layout

- Proper compaction and drainage

- FHA may require a HUD‑approved engineer’s certification if the foundation deviates from standard practice.

Phase 2 – Pre‑Drywall

- FHA requires confirmation that:

- Framing meets structural standards

- Electrical, plumbing, and HVAC rough‑ins comply with code

- Fire‑blocking and draft‑stopping are properly installed

- Weather‑Resistant Barrier (WRB) and flashing are correctly integrated

- Any deficiencies must be corrected before drywall installation.

Phase 3 – Final

- FHA requires the home to meet:

- HUD MPS (Housing and Urban Development – Minimum Property Standards)

- Safety and habitability standards

- Functionality of all systems

- The inspector must confirm:

- Appliances operate

- HVAC is functional

- Hot water is available

- No health/safety hazards exist

- Lender may require a 1004D Final Inspection to certify completion.

🟥 2. VA Loan Requirements

VA = Department of Veterans Affairs

VA follows VA Minimum Property Requirements (MPRs) and focuses heavily on safety, structural soundness, and habitability.

Phase 1 – Foundation

- VA requires the foundation to be:

- Structurally sound

- Free of settlement risks

- Built according to engineered plans

- For new construction, VA often requires:

- Builder certification (formal statement from the builder)

- Engineer’s foundation letter (formal written certification from a licensed professional engineer (PE))

Phase 2 – Pre‑Drywall

- Inspector must verify:

- Structural framing integrity

- Proper installation of mechanical rough‑ins

- Adequate moisture protection (WRB, flashing, roof underlayment)

- VA is strict about:

- Termite protection

- Moisture intrusion prevention

Phase 3 – Final

- VA requires:

- Full compliance with VA MPRs

- All utilities operational

- No safety hazards

- Proper grading away from the structure

- A VA Compliance Inspection Report (Form 26‑1839) may be required.

🟩 3. Conventional Loan Requirements

Conventional loans (non‑government) follow Fannie Mae or Freddie Mac guidelines (Freddie Mac stands for the Federal Home Loan Mortgage Corporation (FHLMC). It is a government‑sponsored enterprise (GSE) created by Congress in 1970 to support the U.S. housing finance system.) depending on the lender.

Phase 1 – Foundation

- Inspector verifies:

- Compliance with local building codes

- Structural adequacy

- Proper reinforcement and plumbing rough‑in

- Engineering certification may be required if the design is non‑standard.

Phase 2 – Pre‑Drywall

- Lenders want assurance that:

- Framing is structurally sound

- Rough‑ins meet code

- Building envelope is properly sealed

- Some lenders require a third‑party inspection report for risk mitigation.

Phase 3 – Final

- Conventional loans require:

- A complete, functional home

- No major defects

- All systems operational

- Typically documented using:

- Appraisal Form 1004D (Completion Report)

- Or a third‑party final inspection report

🟨 4. Fannie Mae (New Construction)

Fannie Mae = Federal National Mortgage Association (FNMA)

Fannie Mae has specific requirements under Selling Guide B4‑1.2‑03.

Phase 1 – Foundation

- Inspector must confirm:

- Foundation built per plans

- Compliance with local code

- Proper drainage and site preparation

- If the foundation differs from plans, an engineer’s certification is required.

Phase 2 – Pre‑Drywall

- Fannie Mae requires verification of:

- Structural framing

- Mechanical rough‑ins

- Weatherproofing and flashing

- Lenders often require a third‑party inspector to reduce construction risk.

Phase 3 – Final

- Fannie Mae requires:

- A completed home meeting all local codes

- Operational systems

- No health/safety issues

- Appraiser must complete:

- Form 1004D to certify completion

- If the home is newly built, a Certificate of Occupancy (CO) is mandatory.

🏗️ Combined Comparison Chart

Organized by Loan Type

🧩 Authorized Inspectors for Each Loan Type

| Loan Type | Who Performs Phase 1–3 Inspections |

|---|---|

| FHA | TREC‑licensed inspectors, HUD‑approved fee inspectors, ICC‑certified inspectors, licensed engineers (if needed), appraiser only for final 1004D |

| VA | TREC‑licensed inspectors, VA‑approved compliance inspectors, licensed engineers (foundation), appraiser sometimes for final |

| Conventional | TREC‑licensed inspectors, independent third‑party inspectors (includes ICC inspectors, engineers, private inspection firms), appraiser for 1004D |

| Fannie Mae | TREC‑licensed inspectors, independent third‑party inspectors, licensed engineers (if deviations), municipal inspector (CO), appraiser for 1004D |

| Freddie Mac | TREC‑licensed inspectors, independent third‑party inspectors, licensed engineers (if deviations), municipal inspector (CO), appraiser for Form 442 (Freddie Mac’s version of the 1004D) |