A New Construction Inspection in Houston, Texas ensures that a newly built home meets safety standards, construction best practices, and builder specifications before closing. Even brand‑new homes can have hidden defects, incomplete work, or installation errors that go unnoticed without a qualified inspector. A professional evaluation helps identify issues early, before they become costly problems for the homeowner.

During the inspection, I examine all major systems and structural components, including the foundation, framing, electrical, plumbing, HVAC, roof, and attic. I look for improper installation, missing components, safety hazards, and workmanship concerns that may affect long‑term performance. This detailed review helps confirm that the home was built correctly and that all visible systems are functioning as intended.

A professional new build home inspection gives buyers confidence, protects their investment, and provides leverage for builder corrections before move‑in. In fast‑growing Texas markets like Houston, a thorough new construction inspection is one of the smartest steps a homeowner can take to ensure quality, safety, and long‑term durability.

🏠 Buyer or Bank‑Required

Grasping these lender expectations helps buyers and builders prevent costly delays and keep projects compliant from the foundation stage through the final walk‑through. Each loan program—FHA, VA, Conventional, Fannie Mae, and Freddie Mac—has its own inspection criteria, and lenders rely on these reports to confirm construction quality and protect the loan. This overview highlights what banks look for and why these inspections play such an important role in the Texas housing market.

FHA, VA, Conventional & Fannie Mae

Understanding Phase 1, Phase 2, and Phase 3 Inspections

Before diving into each loan type, it helps to clarify what “Phase 1, Phase 2, Phase 3” means.

These are NOT federal terms—they are Texas builder/inspector workflow terms used by lenders to verify construction quality before approving a mortgage.

🔧 Texas Construction Inspection Phases (General Definitions)

| Phase | What It Covers | Purpose |

|---|---|---|

| Phase 1 – Pre‑Pour / Foundation Inspection | Soil preparation, formwork, reinforcement, post‑tension cables, plumbing rough‑in | Ensure the foundation is structurally compliant before concrete is poured |

| Phase 2 – Pre‑Drywall / Framing Inspection | Structural framing, roof decking, mechanical rough‑ins (HVAC, plumbing, electrical), window/door installation, WRB, flashing | Verify structural integrity and building envelope before insulation and drywall |

| Phase 3 – Final Inspection | Full home inspection after completion: systems, safety, code compliance, functionality | Confirm the home is complete, safe, and ready for occupancy |

Now, what each loan type requires at each phase.

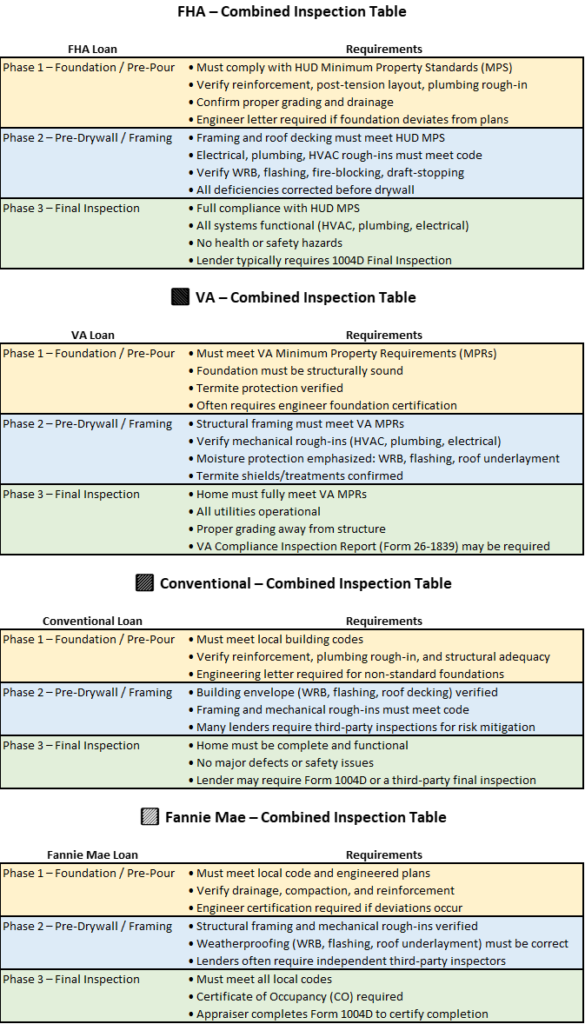

🟦 1. FHA Loan Requirements

FHA = Federal Housing Administration

FHA follows HUD Minimum Property Standards (MPS) and HUD Handbook 4000.1.

Phase 1 – Foundation

- Inspector must verify compliance with HUD MPS and local building codes.

- Special attention to:

- Reinforcement placement

- Post‑tension cable layout

- Proper compaction and drainage

- FHA may require a HUD‑approved engineer’s certification if the foundation deviates from standard practice.

Phase 2 – Pre‑Drywall

- FHA requires confirmation that:

- Framing meets structural standards

- Electrical, plumbing, and HVAC rough‑ins comply with code

- Fire‑blocking and draft‑stopping are properly installed

- Weather‑Resistant Barrier (WRB) and flashing are correctly integrated

- Any deficiencies must be corrected before drywall installation.

Phase 3 – Final

- FHA requires the home to meet:

- HUD MPS (Housing and Urban Development – Minimum Property Standards)

- Safety and habitability standards

- Functionality of all systems

- The inspector must confirm:

- Appliances operate

- HVAC is functional

- Hot water is available

- No health/safety hazards exist

- Lender may require a 1004D Final Inspection to certify completion.

🟥 2. VA Loan Requirements

VA = Department of Veterans Affairs

VA follows VA Minimum Property Requirements (MPRs) and focuses heavily on safety, structural soundness, and habitability.

Phase 1 – Foundation

- VA requires the foundation to be:

- Structurally sound

- Free of settlement risks

- Built according to engineered plans

- For new construction, VA often requires:

- Builder certification (formal statement from the builder)

- Engineer’s foundation letter (formal written certification from a licensed professional engineer (PE))

Phase 2 – Pre‑Drywall

- Inspector must verify:

- Structural framing integrity

- Proper installation of mechanical rough‑ins

- Adequate moisture protection (WRB, flashing, roof underlayment)

- VA is strict about:

- Termite protection

- Moisture intrusion prevention

Phase 3 – Final

- VA requires:

- Full compliance with VA MPRs

- All utilities operational

- No safety hazards

- Proper grading away from the structure

- A VA Compliance Inspection Report (Form 26‑1839) may be required.

🟩 3. Conventional Loan Requirements

Conventional loans (non‑government) follow Fannie Mae or Freddie Mac guidelines (Freddie Mac stands for the Federal Home Loan Mortgage Corporation (FHLMC). It is a government‑sponsored enterprise (GSE) created by Congress in 1970 to support the U.S. housing finance system.) depending on the lender.

Phase 1 – Foundation

- Inspector verifies:

- Compliance with local building codes

- Structural adequacy

- Proper reinforcement and plumbing rough‑in

- Engineering certification may be required if the design is non‑standard.

Phase 2 – Pre‑Drywall

- Lenders want assurance that:

- Framing is structurally sound

- Rough‑ins meet code

- Building envelope is properly sealed

- Some lenders require a third‑party inspection report for risk mitigation.

Phase 3 – Final

- Conventional loans require:

- A complete, functional home

- No major defects

- All systems operational

- Typically documented using:

- Appraisal Form 1004D (Completion Report)

- Or a third‑party final inspection report

🟨 4. Fannie Mae (New Construction)

Fannie Mae = Federal National Mortgage Association (FNMA)

Fannie Mae has specific requirements under Selling Guide B4‑1.2‑03.

Phase 1 – Foundation

- Inspector must confirm:

- Foundation built per plans

- Compliance with local code

- Proper drainage and site preparation

- If the foundation differs from plans, an engineer’s certification is required.

Phase 2 – Pre‑Drywall

- Fannie Mae requires verification of:

- Structural framing

- Mechanical rough‑ins

- Weatherproofing and flashing

- Lenders often require a third‑party inspector to reduce construction risk.

Phase 3 – Final

- Fannie Mae requires:

- A completed home meeting all local codes

- Operational systems

- No health/safety issues

- Appraiser must complete:

- Form 1004D to certify completion

- If the home is newly built, a Certificate of Occupancy (CO) is mandatory.

🏗️ Combined Comparison Chart

Organized by Loan Type

🧩 Authorized Inspectors for Each Loan Type

| Loan Type | Who Performs Phase 1–3 Inspections |

|---|---|

| FHA | TREC‑licensed inspectors, HUD‑approved fee inspectors, ICC‑certified inspectors, licensed engineers (if needed), appraiser only for final 1004D |

| VA | TREC‑licensed inspectors, VA‑approved compliance inspectors, licensed engineers (foundation), appraiser sometimes for final |

| Conventional | TREC‑licensed inspectors, independent third‑party inspectors (includes ICC inspectors, engineers, private inspection firms), appraiser for 1004D |

| Fannie Mae | TREC‑licensed inspectors, independent third‑party inspectors, licensed engineers (if deviations), municipal inspector (CO), appraiser for 1004D |

| Freddie Mac | TREC‑licensed inspectors, independent third‑party inspectors, licensed engineers (if deviations), municipal inspector (CO), appraiser for Form 442 (Freddie Mac’s version of the 1004D) |

🛡️ Home Insurance Company Inspections

Home insurance companies perform inspections to assess the overall risk of a property before issuing or renewing a policy. Unlike lenders—who focus on construction progress and loan protection—insurers concentrate on identifying potential hazards that could lead to future claims. Their primary goal is to determine whether the home is insurable, what premium to assign, and whether any repairs or improvements are necessary to reduce risk.

What Insurers Look For

Insurance inspections typically evaluate the condition, safety, and remaining life expectancy of major systems. Common areas of review include:

- Roof Condition: Inspectors look for damage, aging materials, missing shingles, leaks, and overall life expectancy.

- 4‑Point Inspection: A focused review of the roof, HVAC system, plumbing, and electrical components to identify safety concerns or outdated systems.

- Exterior and Interior Risks: Signs of water intrusion, structural issues, improper drainage, or hazards that increase the likelihood of claims.

- Windstorm or Coastal Requirements: In certain regions, insurers may require specialized inspections or certifications to verify compliance with windstorm standards.

Who Performs These Inspections

Insurance companies typically hire their own contracted inspectors, adjusters, or third‑party professionals to evaluate a property.

However, if you are shopping for home insurance, you can request an inspection from us before the insurance company sends their own inspector.

This gives you confidence and peace of mind, helping you identify potential issues in advance so there are no unexpected surprises during the insurer’s review.